$11BN Sinomine raises US$764M to fund Zambian copper expansion ~4km away from PAT

Earlier in the week we saw the following news in Bloomberg:

“China’s Sinomine Resource Group is seeking as much as 5.2BN yuan (US$764M)” to fund its African mining projects.

And we noticed a chunk of the funding was going to fund expansions of Sinomine’s copper mine in Zambia (the Kitumba project).

(source)

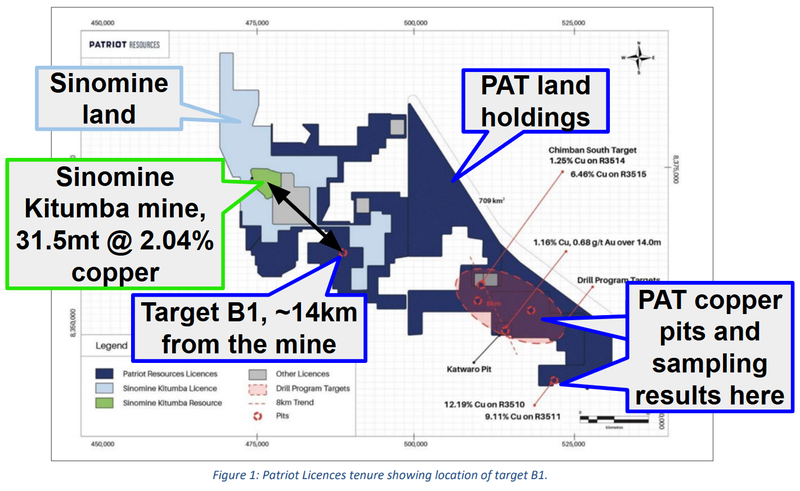

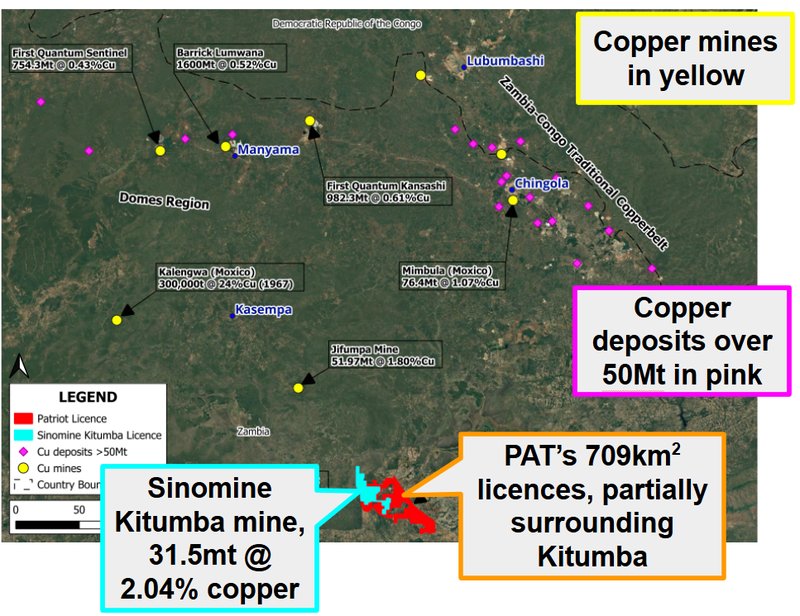

The same project that sits ~4km away from our Investment Patriot Resources (ASX: PAT).

PAT actually holds land surrounding the mine itself:

(source)

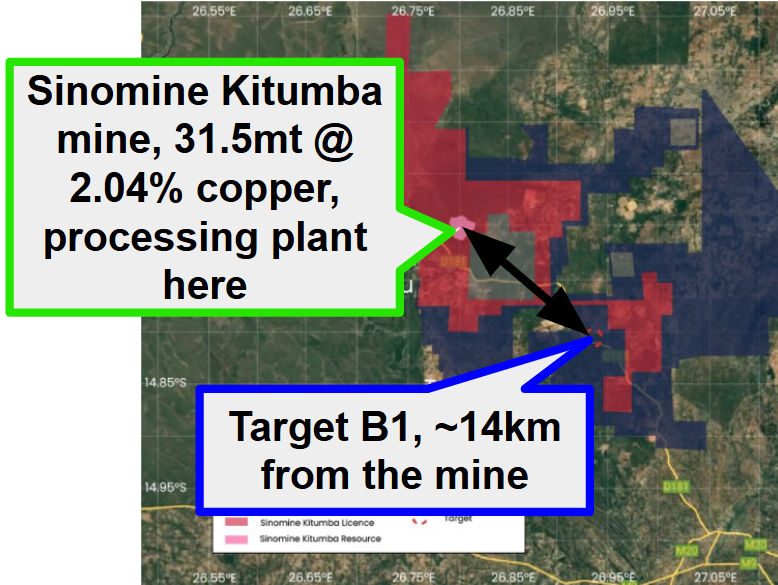

Here is a zoomed in version showing just how close PAT’s B1 target is to where Sinomine are building their processing plant:

(source)

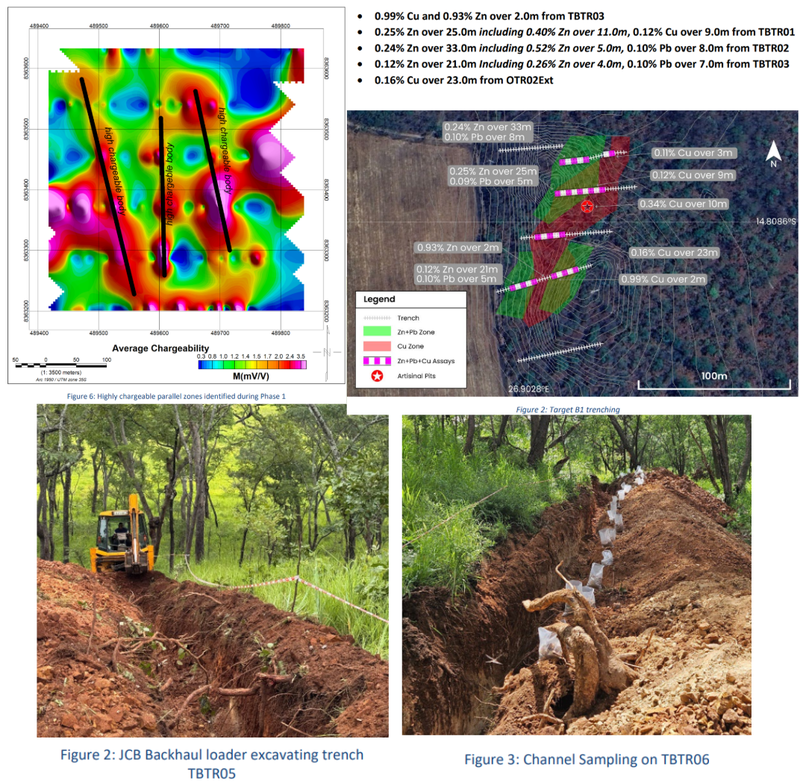

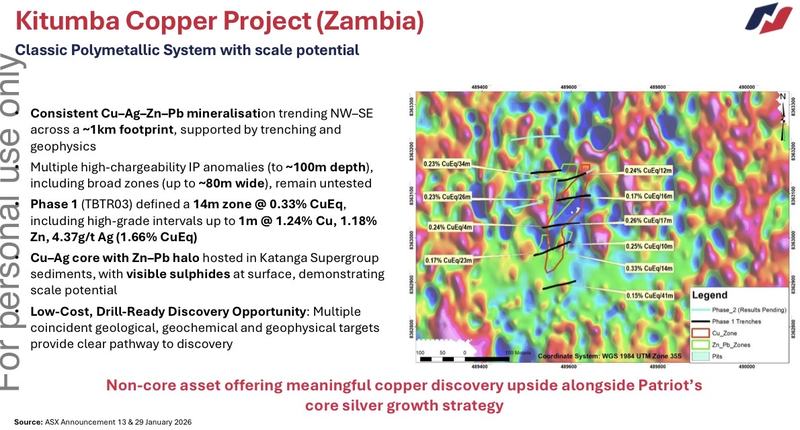

The B1 target is where PAT has actually run two rounds of trench sampling (returning grades up to 0.99% copper) AND multiple rounds of geophysics to identity 400m+ target areas:

A part of the Sinomine raise was set aside to speed up the ramp-up of its project - to a run rate of ~38,000 tonnes of copper annually over 15 years.

The Kitumba processing plant is scheduled to come online in late 2026.

Here is PAT’s Managing Director Dominic overlooking the construction happening on Sinomine’s ground:

(source)

We think this sort of expansion so close to PAT’s ground makes its copper project a lot more interesting.

We are Invested in PAT for its silver project in Peru.

BUT it's hard for this copper asset to not occupy part of our brains when Sinomine is this active next door.

Especially considering the project has multiple IP anomalies that are untested.

AND phase 1 drilling hit copper 14 -5 0.33% copper equivalent) over a few hundred metre area:

AND the number of 50mt+ copper deposits in the region:

(source)

IF PAT was to find anything remotely close to the 1-2% copper grades at scale then it very quickly makes its project an acquisition target for someone like a Sinomine.

After all, Sinomine is spending hundreds of millions on building processing infrastructure that they will ultimately want to run for as long as possible (so any new feed sources would be attractive to them).

The PAT x Sinomine connection

Another reason we think the nearology to Sinomine matters is because of the history PAT’s chair Hugh Warner has with them.

Hugh was a co-founder of Prospect Resources that picked up the Arcadia lithium project in Zimbabwe, made the discovery, and sold it to a Chinese major (Huayou Cobalt) for US$378M.

Prospect went from a $6M market cap micro-cap to a US$378M cash pay day under that team.

Arcadia is now the largest operating lithium mine in Africa.

During that time Hugh actually dealt directly with Sinomine, (share placements and 2 offtake agreements):

(source)

So we have:

- PAT’s Chairman with a direct track record of building African mineral assets and selling them to Chinese majors at scale

- A PAT copper asset sitting 4km from a Chinese major (Sinomine) ramping up its own Zambian copper development

- Sinomine having dealt directly with PAT’s chair during his time at Prospect Resources.

There’s no guarantee anything happens between PAT and Sinomine - but the set-up is conveniently similar to the kind of playbook Hugh has run before.

A reminder - we’re mainly invested in PAT for the silver

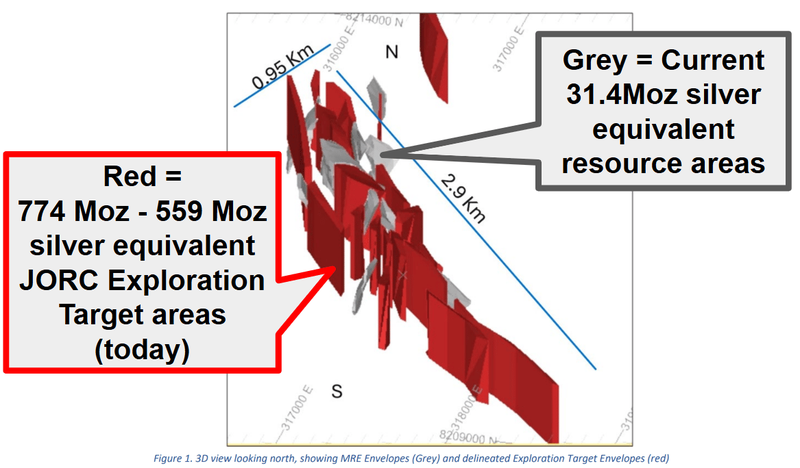

PAT’s Peruvian silver project has a JORC exploration target of up to 774Moz silver equivalents.

Large enough to be one of the largest undeveloped silver systems globally.

(source)

The exploration target is based on an integrated model showing:

- A structure that 2,880m north-south by ~950m wide, down to ~550m depth.

- Has 19 mineralised zones across the corridor (the current 31.4 Moz Inferred Resource is in just 3 of them)

- 479 to 663 Moz of silver at 42-49 g/t - confirming the project is a silver-dominant system.

- 1,832 surface samples, 8,500m of historical diamond drilling

- ~36km IP geophysics,

- ~70km ground magnetics

Of course there’s some caveats with Exploration Targets - they are NOT mineral resources, the drilling rig is required to prove the accuracy of this exploration target.

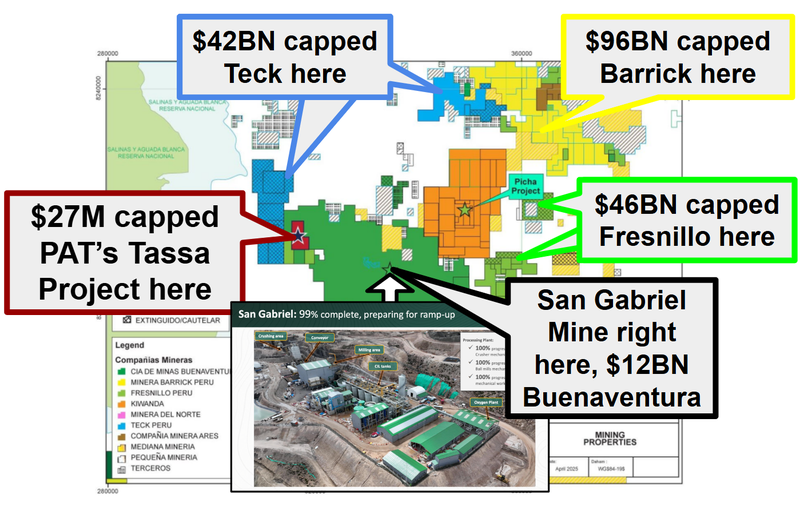

PAT also has some good company in the area also:

(source)

We covered that here: PAT: Up to 774 Million oz silver Eq JORC exploration target - one of the largest undeveloped silver systems globally.

What do we want to see PAT do next?

Drill and update the current silver resource

We want to see PAT drill its silver project in Peru and confirm the existing 31.4M ounce silver equivalent JORC resource.

With the first program, we want to see the previous results confirmed with infill drilling.

Milestones:

🔲 Phase 1 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource.

Drill and grow the current resource

Once PAT has run some infill drilling campaigns, we will be looking for PAT to do some exploratory drilling by stepping out and testing extensional/deeper targets.

That’s where we are hoping PAT grows its current 31M oz silver equivalent resource to the upper end of its 87M ounce silver equivalent exploration target.

By growing the resource PAT will be able to be better compared to its other silver peers on the ASX.

Recently PAT announced an exploration target with an upper end around 9x the current resource, so we need drilling to see if this becomes a reality.

Milestones:

🔲 Phase 2 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource (target: 50M+ silver equivalent ounces)

(Bonus): Sell non-core assets

We think PAT could also unlock capital for its silver asset in Peru by spinning out its projects in Zambia and Canada. Any deal here would be a bonus.

(PAT has a copper asset in Zambia and a lithium asset in Canada).